Section 179 and 100% Bonus Depreciation in 2026: Finance the Equipment Now, Deduct It This Year

Here's the part most business owners don't realize until their accountant tells them in March, when it's too late to do anything about it:

You can finance a piece of equipment, put a fraction of its cost down, and still deduct the entire purchase price this year.

Not the down payment. Not this year's payments. The whole thing.

That's not a loophole. It's how Section 179 and bonus depreciation have worked for years, and in 2026 the numbers are the most generous they've ever been. The only real constraint is the calendar — and the calendar is not on your side after about mid-November.

The 2026 numbers

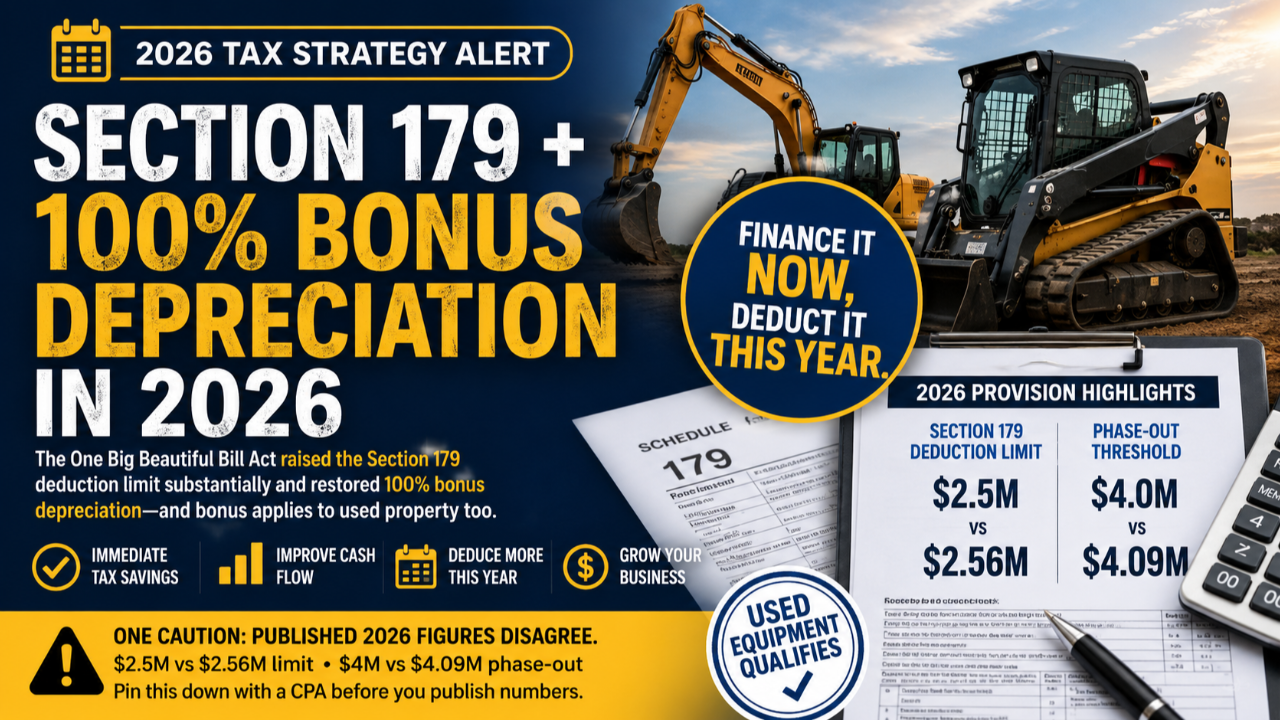

The One Big Beautiful Bill Act, signed in July 2025, made two changes that matter enormously to anyone buying equipment:

Section 179 expensing. OBBBA raised the maximum deduction from $1 million to $2.5 million and the phase-out threshold from $2.5 million to $4 million — permanently, and indexed to inflation. After the IRS inflation adjustment in Rev. Proc. 2025-32, the 2026 figures are:

| 2026 | |

|---|---|

| Maximum Section 179 deduction | $2,560,000 |

| Phase-out threshold | $4,090,000 |

| Fully phased out at | $6,650,000 |

| Heavy SUV cap (6,000–14,000 lbs GVWR) | $32,000 |

100% bonus depreciation is back. It had been phasing down — 80%, then 60%, on its way to zero. OBBBA restored it to 100% for qualifying property acquired and placed in service after January 19, 2025, and made it permanent. There's no dollar cap on bonus depreciation.

For the overwhelming majority of businesses reading this, the practical translation is simple: if you buy qualifying equipment in 2026 and put it to work in 2026, you can almost certainly write off 100% of it in 2026.

The part that actually matters: you don't have to pay cash

This is where financing changes the arithmetic entirely.

The tax code doesn't care how you paid for the equipment. It cares that you acquired it and placed it in service. Whether the cash came from your bank account, a bank loan, or an equipment finance contract, the deduction is the same.

So consider two businesses that both buy a $150,000 machine in October:

Business A pays cash. They're out $150,000 today. They deduct $150,000. At a 32% effective rate, that's roughly $48,000 back at tax time. Net cash out in year one: about $102,000 — and their bank balance took a $150,000 hit in the meantime.

Business B finances it. They put nothing down, start payments in January under a deferred structure, and pay maybe $9,000 across the remainder of 2026. They deduct the same $150,000. Same roughly $48,000 in tax savings. Net cash position in year one: they're ahead — the deduction exceeds what they've paid out.

Same machine. Same deduction. Wildly different cash flow.

That's the whole argument, and it's why the phrase "finance it now, deduct it this year" isn't marketing copy. It's just what the numbers do.

(These figures are illustrative. Your actual result depends on your tax rate, your taxable income, and your specific structure — talk to your CPA.)

Used equipment counts

Worth saying loudly, because a lot of business owners assume otherwise: both Section 179 and 100% bonus depreciation apply to used equipment.

For bonus depreciation, the requirement is that it's first use by your business — not that the equipment rolled off the line new. A five-year-old excavator you bought at auction qualifies. A well-maintained used box truck qualifies. A refurbished CNC machine qualifies.

This matters because used equipment is frequently the smarter buy — half the price, most of the useful life, and the same first-year write-off. The tax code doesn't penalize you for being sensible about it.

Section 179 vs. bonus depreciation — do you need to pick?

Usually not. Most businesses use both, in order.

Section 179 is an election. You choose it, asset by asset, and you control how much you take. Its main limitation: your Section 179 deduction can't exceed your business's taxable income. If you had a thin year, your deduction gets capped — though the unused portion carries forward indefinitely.

Bonus depreciation applies automatically to eligible property unless you elect out. It has no dollar cap and no taxable income limitation, which means it can create or deepen a net operating loss.

The common approach: elect Section 179 on the assets where you want precise control, then let 100% bonus depreciation soak up whatever basis remains. In a normal profitable year, this gets you to a full write-off either way.

Where it gets genuinely strategic is in unusual years. Thin income year? You might lean on bonus depreciation now and preserve Section 179 for a stronger year. Expecting a big year in 2027? Timing matters. This is a real conversation to have with your accountant, not a box to check.

The deadline that trips people up

Placed in service by December 31. Not ordered. Not paid for. Not sitting on a truck somewhere in Ohio.

The equipment has to be delivered, installed, and ready and available for its intended use before the year ends. A machine that arrives December 28 and gets commissioned January 6 is a 2027 deduction, no matter when you signed the contract or wrote the check.

Which is why the real deadline isn't December 31 — it's whenever your lead time says it is. If your equipment takes six weeks to build and two weeks to install, your actual cutoff is early November. Popular equipment gets scarce in Q4 for exactly this reason: everyone figures this out at the same time.

Financing is rarely the bottleneck. Applications take minutes, approvals often come back within hours, and funding can follow in as little as 24 hours. The bottleneck is almost always the equipment itself. Get the financing settled early so it's not the thing standing between you and a delivery slot.

A few things to verify with your CPA

We're a finance company, not a tax firm, and the honest answer to most tax questions is "it depends on your situation." Specifically:

- State conformity varies. Federal Section 179 rules apply nationwide, but states differ — some match federal treatment, some limit it, some decouple entirely.

- Business-use percentage matters, particularly for vehicles. Drop below 50% business use in a later year and you may face recapture.

- The taxable income limitation on Section 179 is at the entity level and can flow through to owners in ways that surprise people.

- Vehicles have their own rules. Heavy SUVs are capped. Vehicles under 6,000 lbs GVWR face much tighter limits. Trucks with beds six feet or longer generally escape the SUV cap.

- Section 179 is use-it-or-lose-it on the original return. If you don't elect it when you file, you generally can't go back and claim it later.

Where to start

If there's equipment you already know you need — the machine you've been nursing along, the truck you keep renting, the line you've been meaning to expand — 2026 is a genuinely good year to stop deferring it. The deduction is at its maximum, bonus depreciation is at 100%, and financing means the write-off can land before most of the cost does.

The order of operations is straightforward:

- Get quotes and confirm lead times. This is your real deadline.

- Get financing approved. Minutes to apply, often hours to an answer.

- Call your CPA with the actual numbers before you sign.

- Take delivery and get it running before December 31.

Everlasting Capital finances new and used equipment from $1,000 to $2,000,000 — machinery, commercial vehicles, technology, shop equipment, medical and dental — with terms up to 60 months, deferred payment options, and up to 100% financing that can include shipping, taxes, and installation. We work with businesses across every credit profile, in all 48 continental states.

See what you qualify for at everlastingcapital.com/apply

It takes a few minutes, and it costs you nothing to find out where you stand.

Everlasting Capital is not a tax advisor and this article is not tax advice. Figures reflect IRS Rev. Proc. 2025-32 for tax years beginning in 2026 and are subject to change. Consult a qualified tax professional about how Section 179, bonus depreciation, and state conformity apply to your business. Financing terms, amounts, and approval times vary by program, credit profile, and equipment type.